Co-authored by Alissa Doherty, Jason Humm, and David Yardley.

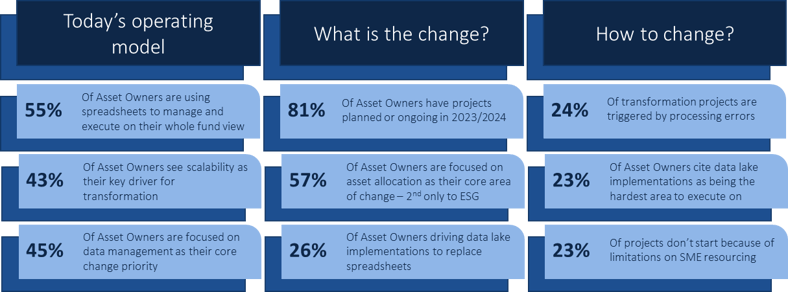

This year, we worked alongside industry partners to distribute a global survey to asset owners delving into changes, challenges, and trends in their operating model and investment operations. Early results from our 2023 Citisoft Asset Owner Survey discovered the following:

- 55% of asset owners are using spreadsheets to manage and execute on their whole fund view

- 57% of asset owners are focused on asset allocation as their core area of change–second only to ESG

- 45% of asset owners are focused on data management as their core change priority

The above survey takeaways reflect what most of us likely know and are experiencing:

- Achieving a centralized view across all asset classes managed by an organization remains extremely difficult. This is primarily due to the challenge of data provision for alternatives and other complex asset types like swaps and bank loans.

- Most organizations are attempting to achieve a holistic view of their portfolios by loading data from disparate sources into either Excel or some form of data warehouse or lake. Unfortunately, loading the data is the easy part. Consolidating, classifying, and reporting on that data remains a huge challenge.

- Asset allocation—a key area of change for 57% of respondents—is currently lacking. One significant reason is because all assets are not in the same place, which makes achieving asset allocation across all portfolios very difficult to achieve.

- Improvements in “data management” are viewed as key in the support of operations. We should define this requirement with slightly more granularity: data consolidation and data classification are really the key—without these the data can’t be accessed or used.

Key factors to achieving a consolidated view across portfolios

What do we need to do in order to solution for the above high-level problems? The focus for many asset owners—and asset management vendors and service providers—is a centralized platform supporting business functionality across all asset classes.

What would we identify as some of our key functional requirements for such a solution? Though this may be an aspirational list, our key requirements would likely include those identified in the table below:

|

Core Requirement |

Description |

|

Multi-asset class functionality |

Support for all asset classes—public markets, derivatives, and alternatives—e.g., allocation, risk management, performance measurement and attribution, reporting |

|

Centralized, single source of the truth |

Replacement of current siloed, asset-class based systems with a single, centralized platform across all domains and asset classes |

|

Timely and accurate data |

Accurate, timely books of record |

|

Rich portfolio management toolset |

Provision of tools to support portfolio analysis and decision-making on the same platform as the centralized, underlying data |

|

Support for the full investment lifecycle, from front to back |

Moving from segregated front, middle and back office systems and operational processing to a solution supporting the full investment lifecycle of an instrument or transaction, from start to finish, on a single, centralized platform |

|

Systemization and automation |

Elimination of manual processing via utilization of process automation, machine learning, and artificial intelligence |

Data: the heart of the solution, but the root cause of so many problems…

Drilling down further into the key requirements for a holistic view across portfolios, we can identify data as the core of the required solution. The diagram below depicts the “day in the life” business processing for investment management operations.

As mentioned above, data is also at the base of many of our problems:

|

Core Data Issue |

Description |

|

Availability |

|

|

Quality |

|

|

Granularity |

|

|

Provision and Classification |

|

|

Operational Processing |

|

|

Flexibility and Scalability |

|

|

Cost |

|

Current industry solutions aimed at achieving a consolidated view across portfolios

What initiatives are we seeing in our asset management industry that aim to solution for a consolidated view across all of our portfolios and operations? Particularly given that the once standard business model for many asset owners is now transforming—for example with major insurance companies expanding to include alternatives, and public pension plans more closely resembling investment management organizations with holdings across all asset classes.

Single database solutions

There are a small number of vendors who have built their solutions on a single database model, supporting all asset classes, with associated business processing. These vendors have faced down the rhetoric that they don’t have the extent of functionality of best of breed providers, such that a single platform can be seen as a compromise. The recent drive towards centralized platforms supporting all asset classes and processing is justifying the single database platform model. The question is whether these systems are fully ready to support a consolidated portfolio view and front to back operational processing.

Front to back platforms

A number of the major players in the service provider marketplace have come to market with offerings that support all asset classes and associated investment lifecycle processing, “front to back.” Are these “centralized” platforms? Technically not, but if engineered and solutioned well, they can support the requirements of a consolidated portfolio view.

The reality of achieving a consolidated view

The truth is that a platform that fully supports a consolidated, multi-asset portfolio view, with associated front to back processing, is still a unicorn. There is movement in the right direction, but anyone embarking on a journey to implement a consolidated portfolio view is looking at a multi-year roadmap that involves a lot of build, large amounts of money, and not a small amount of frustration and failure.

Facing this reality, what can we do in the interim? Listed below are initiatives that will at least position us while we wait for that ultimate silver bullet.

Get SaaSy

Any new initiatives—even interim state—should ideally be SaaS based—Software as a Service. Why? Maintenance, support, upgrades, flexibility, ability to scale….

If you want to dig deeper into SaaS and digitalization, take a look at this article on key opportunities and the steps firms need to take to be change-ready: Innovation in SaaS and Digitalization.

Think cloud and Snowflake

One approach to a consolidated view across all portfolios has been the data warehouse—bringing together data from various best of breed systems into one central data repository, for centralized business processing and reporting.

One of the major problems with the previous generation of data warehouse solutions was processing time. It took hours for batch cycles to run and load data into the data warehouse. Snowflake, and other cloud-based data technology, is beginning to solve this processing time/capacity issue. With the cloud, and with as an example the Snowflake Marketplace—where data providers can present their data sets as available to Snowflake business users—the potential to solution a consolidated portfolio view is huge.

Use AI

It’s time to use AI. Advances in artificial intelligence and machine learning are helping to make unstructured data collection more efficient and precise. Much of the critical business data for alternatives is traditionally delivered via documents. Pulling the required data from these documents is typically manual, time consuming, and carries a high level of risk due to manual error. Machine learning is advancing to the point where the technology can systematically read, digitize, and load data into a system or database. For more, on this topic, take a look at the excellent article written by our colleague Chris Mills on AI: More Intelligence Needed in Asset Management.

Undertake due diligence

If we really are going “all in” on that target state front to back multi-asset investment management platform, we need to do our due diligence. There are a lot of great front to back platform models and marketing materials out there. But we need to look closely before making such a huge decision. If we are going to enter into a 5 to 10 year program to implement and use a target state platform, we can justify a detailed and thorough evaluation and due diligence process. A couple of workshops is not going to do it. All that glitters is not gold. Look under the hood/bonnet, take it for a test drive. If the engine isn’t ready yet, or it only has two wheels, you know you have a difficult journey ahead.

Consider your service provider model

Most asset managers will have some level of relationship with—and dependency on—a service provider. We are talking custodians, vendors, fund administrators, middle office service providers and similar.

Improving the service provider relationship and model, whilst driving improvements in operational processing, will lead to incremental productivity improvements and cost savings—with only a fraction of the cost and effort of replacing whole platforms and operating models. Speak with your service providers, find out their latest model improvements, look at their target roadmap, and see where your organization can benefit and make improvements.

Sometimes we can’t have it all, neatly bundled, right away. That all-in-one front to back multi-asset platform is coming, but it may be a while. In the interim, it makes sense to focus on iterative improvements—the sum of which could be quite significant—with much less cost, and with significantly less risk.

.png?width=200&height=200&name=Blog%20-%20Featured%20Images%20-%20500%20x%20500%20(15).png)

.png?width=200&height=200&name=Blog%20-%20Featured%20Images%20-%20500%20x%20500%20(9).png)

Comments