Inflation concerns are rising

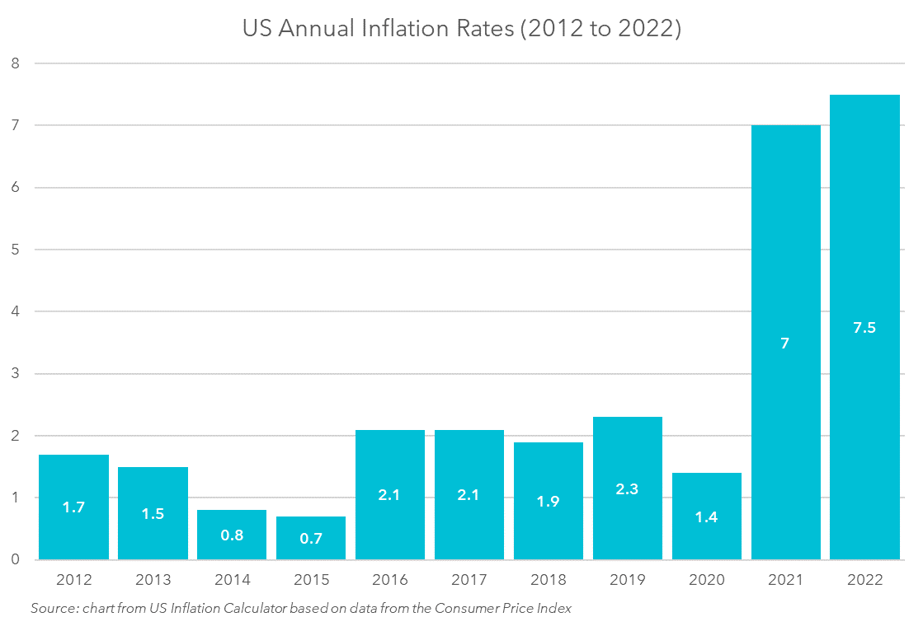

The word ‘inflation’ may have more mentions in the past ten months than the previous ten years combined. The recent spike is a stark contrast to the past few decades which have been quite favorable in terms of US. inflation. There are now multiple generations of investors who have not experienced significant inflation and its erosive impact upon their portfolios, as well as their day-to-day lives. The average annual inflation rate from 1991-2020 was a modest 2.25% which was generally unremarkable. In 2022, inflation concerns have reached fever pitch. While we do not know the level of inflation that awaits us, we do know that it is prevalent, and its current pace is hastening along with fears of deteriorating market conditions.

The Federal Reserve (Fed) has the onerous (and unenviable) task of ensuring that inflation remains within an acceptable range. The Fed had officially stated (prior to the Russian invasion of Ukraine of course) that this current high-inflationary period is likely transitory and therefore should return to moderate levels in the near term. However, many others are less convinced of this optimistic outlook, even though the Fed has a proven decades-long track record to boast about.

One thing that we do know for certain is that investors will become more interested in measuring the inflationary impact upon their investments. The mechanism typically used is an inflation-adjusted real return measure which is a gauge to remove the effect of inflation to reveal earnings potential. Inflation is calculated using the Consumer Price Index (CPI) as a monthly factor and applied across all returns, but the impact is not felt with equal severity or magnitude across investments; a real rate of return measure may help identify investment risks as well as opportunities.

This begs the question of whether real returns deserve more attention and if they should be shown with equal prominence to nominal returns in performance reporting and disclosures.

Impacts are not created equal

A key argument for presenting real returns on investment products is an impending need to provide investors with a comparative tool to assess investments strategies and products during high-inflation periods. For illustrative purposes, in 1979 the S&P 500 had a total return of 18.5% which sounds great, but inflation was 13.3% so the real return would have been a modest 5.2%. Which return would investors deem to be more relevant to their goals and fortunes? The 1979 portfolio may have increased at twice the average historical S&P 500 return, but its purchasing capabilities were approximately half of the average return for that year. Inflation rates from 1978 to 1981 were between 8.9% and 13.3%. Performance reporting should appropriately reflect significant inflationary impact to give readers of financial information this alternate view of their returns.

From a specific (micro) perspective, inflationary impacts are felt differently across asset classes, industries, sectors, individual companies, and ultimately individual investors. These impacts depend upon several factors such as the ability of firms to impose pricing power versus firms subjected to pricing pressure. Capital structures inclusive of debt-to-equity and method of funding operations will also create uneven experiences. Equity-heavy firms will be impacted differently from debt-heavy firms, and fixed-rate debt will behave differently from variable-rate debt. There are traditional safe havens such as gold, real estate investment trusts (REITS), and equities; but the exposures for each competitor within these havens will be different.

We also cannot assume that tightly coupled competitors will feel identical impacts. As examples, will inflationary impacts be the same for Ford and GM, FedEx and UPS, Exxon Mobil, and Chevron? These firms are uniquely financed, and each possesses different pricing power. To demonstrate further, consider that each household will not be impacted equally during inflationary periods. Some individuals have income associated with growth, and some have no debt or fixed rate debt to insulate them from increased exposure or risk.

If impacts are not felt consistently, then assessing portfolio managers for strategies that will be inflation-resistant is essential to finding the best match of risk profile of each investor.

Performance and standardized inflation reporting

As investors become more concerned that inflation is eroding invested assets, then let’s take the proactive approach and enable investors with real returns to better assess results across their portfolios. This information will provide investors with the critical insight necessary to inform future decisions. Longer-term and retirement-focused investors will typically receive the greatest benefit of real returns as they assess performance along the statutory performance reporting periods of one, three, five, and 10 years.

Regulatory bodies such as the Securities and Exchange Commission (SEC) and investment industry groups such as CFA Institute (via Global Investment Performance Standards aka GIPS) are focused on presenting performance in a fair, ethical, and standardized framework. Changes throughout time have included standardized calculations, time-periods, net-of-fee returns, after-tax returns, return-of-capital disclosures, and many others. This may be the right time to consider the inclusion of real returns within standardized reporting and disclosures. Educating and informing investors is a cornerstone to the SEC and CFA Institute mission, and the presentation of real returns with equal prominence will be consistent with that mission.

Performance reporting is intended to inform and provide a comparative platform for investors. Identifying managers and strategies that can navigate a high-inflation environment will become more important to investors if inflation persists and finding portfolio strategies and managers that can navigate inflationary markets is more important today than it has been in the recent past.

“The real voyage of discovery consists, not in seeking new landscapes, but in having new eyes” – Marcel Proust

.png?width=200&height=200&name=Blog%20-%20Featured%20Images%20-%20500%20x%20500%20(6).png)

.png?width=200&height=200&name=RBCIS%20(2).png)

Comments